Pound tumbles as recession fears grow after UK economy shrinks by 0.3% in April

GDP falls faster than experts had forecast as government cuts back on Covid spending and manufacturers are hit by higher prices

The pound fell against the dollar and UK stock markets tumbled on Monday after gloomy figures showed the country was edging closer to a recession.

The economy shrank unexpectedly in April amid spiralling prices for essential goods, rising interest rates and record fuel costs.

Experts said the data was now catching up with the “cocktail of challenges” that the UK faces, with the potential for further problems as trade relations with the EU deteriorate.

Official figures showed that the UK’s gross domestic product (GDP) – a measure of the total goods and services produced – had fallen by 0.3 per cent in April, following a 0.1 per cent contraction in March and zero growth in February.

Markets reacted strongly to the news, with London’s FTSE 100 index of leading shares dropping 1.5 per cent and the pound falling 1.5 cents against the dollar. Sterling was trading at $1.216 when the London Stock Exchange closed for the day.

Across the Atlantic, Wall Street screens flashed red as the S&P 500 opened down again, losing 2.4 per cent of its value in morning trading.

The index is now in a bear market, having lost a fifth of its value since the recent high reached in January. The tech-focused Nasdaq has now lost more than 30 per cent of its value since its recent peak.

High-growth technology stocks such as Peloton and Zoom have taken a pummelling in recent weeks, erasing huge gains made during the early part of the pandemic.

The sell-off has come as central banks hike interest rates in a bid to cool the economy and slow down the rate of price increases.

Fears are growing that central banks will have to act more hawkishly, or inflation will soon be difficult to control.

April saw UK domestic energy bills jump by 54 per cent at the same time as workers were hit with a national insurance hike. Meanwhile, food and fuel prices have surged following major disruuption to supplies in the wake of Russia’s invasion of Ukraine.

The Office for National Statistics (ONS) said on Monday that the UK’s GDP was now 0.9 per cent above its pre-pandemic level, but 0.4 per cent below the peak reached in January. Experts had been expecting a 0.1 per cent rise in GDP in April.

The ONS said it marked the first time GDP had fallen for two months in a row since March and April 2020, when the pandemic first hit and sent the economy tumbling.

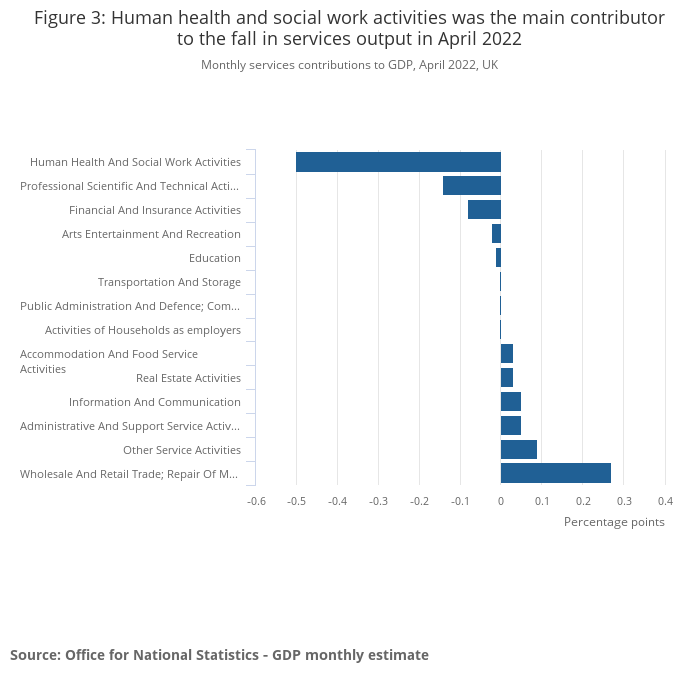

Output contracted by 0.3 per cent in the services sector, which makes up more than three quarters of the UK economy. This was largely due to the ending of the government’s Covid-19 Test and Trace programme, and lower vaccination activity.

Ending free testing shaved 0.5 percentage points off GDP. With the test and trace and vaccines impact stripped out, output would have risen by 0.1 per cent in April, the ONS said.

Activity also fell in the two other major parts of the economy. Manufacturing shrank by 1 per cent as firms reported being hit hard by big price rises and delays to supplies. Construction output fell by 0.4 per cent.

Last week, the OECD group of wealthy nations unveiled forecasts predicting that the UK would fall behind every other developed economy except Russia next year, as growth falls to zero.

Analysts were divided on the question of whether the UK would avoid a recession, which is defined as two successive quarters of negative economic growth.

Martin Beck, chief economic adviser to the EY Item Club, said the outlook was poor.

“An already serious squeeze on households’ spending power will be negatively affected by the inflationary impact of global supply chain frictions and sterling’s recent weakness,” he said, adding that UK interest rates were likely to rise again later this week.

The Bank of England is set to announce its latest interest rate decision on Thursday, with markets expecting a further rise.

The Bank’s Monetary Policy Committee is seeking to tame inflation, which is forecast to hit 10 per cent later this year, well above the 2 per cent target rate.

Further increases will further eat into household budgets, and are expected to slow consumer spending, which will drag on the wider economy.

Samuel Tombs, chief UK economist at Pantheon Macroeconomics, said private sector activity had helped to offset a sharp fall in Covid-related government spending and “renewed weakness” in manufacturing. However, a recession remains unlikely, he said.

“Households’ real disposable incomes should rise in both the third and fourth quarters now that the chancellor has announced an extra £5bn in grants during these quarters, equal to nearly 2 per cent of their likely income in these quarters.

“So provided energy prices rise no further, and households start to draw cautiously on their savings, we look for quarter-on-quarter GDP growth of about 0.6 per cent in the third quarter and 0.5 per cent in the fourth quarter,” he added.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments